Key Highlights

- A short sale in real estate means selling your home for less than your remaining mortgage balance, with the mortgage lender’s approval, when you can’t keep up with mortgage payments. For sellers, the main steps in the short sale process include contacting your lender to discuss your financial situation, submitting a hardship letter and supporting documentation, listing the property with a real estate agent, receiving and negotiating offers, and then awaiting lender approval for the chosen offer. For buyers, the process involves submitting an offer, waiting for the seller’s lender to review and possibly approve the offer, and then proceeding with the regular closing steps if approval is granted.

- Both short sales and foreclosures impact your credit score, but a short sale usually causes less credit damage than the foreclosure process. However, buyers considering a short sale should watch out for potential delays in the approval process, as lenders must approve the sale, which can take additional time compared to traditional real estate transactions. It’s also important to be aware of the property’s condition, as short sale homes are often sold “as is,” and there may be outstanding liens or financial obligations attached to the property.Creative financing, like “subject-to” real estate deals, offers alternatives to the traditional short sale route and can help homeowners avoid foreclosure altogether.

- Creative financing, like “subject-to” real estate deals, offers alternatives to the traditional short sale route and can help homeowners avoid foreclosure altogether. For Florida homeowners facing foreclosure, understanding short sales is crucial—a short sale occurs when you sell your home for less than the amount owed on your mortgage, requiring lender approval. While a short sale may help avoid foreclosure, it can negatively impact your credit score, though typically less severely than a foreclosure itself. Market conditions, declining home values, and personal financial hardship are common reasons homeowners consider short sales.As an alternative, “subject-to” real estate allows buyers to take over your existing loan payments—potentially preserving your credit and offering a faster, less damaging solution. EPS Houses specializes in helping Florida homeowners review their options, including creative real estate strategies, to avoid foreclosure and minimize risks to their financial future.

- Market conditions, declining home values, and personal financial hardship are common reasons homeowners consider short sales.

- EPS Houses helps homeowners use subject-to real estate transactions to stop foreclosure, protect their credit, and avoid the lengthy short sale process.

Introduction

Navigating the world of real estate can be tough, especially when financial hardship makes it difficult to pay your mortgage. If you’re facing the risks of a short sale or foreclosure, you might feel like you’re out of options. The short sale process can be complex, and the foreclosure process can severely impact your financial future. However, there are creative solutions that can help you avoid a short sale and protect your credit. This guide explains your options, including how subject-to real estate can offer you a fresh start.

In this blog, we’ll compare short sales and subject-to deals to help you understand their pros and cons. Short sales often require lender approval, potentially damage your credit, and may result in the sale of your house for less than you owe—leaving you with little or no equity. In contrast, subject-to deals allow you to transfer ownership while keeping your existing mortgage in place, which can be quicker, protect more of your equity, and have less impact on your credit. Selling subject-to with EPS Houses is a stronger long-term solution for avoiding foreclosure, as it helps preserve your financial stability and protects your equity better than a traditional short sale.

Understanding Short Sales and Foreclosures

A homeowner thinking about solutions

Understanding the differences between a short sale and the foreclosure process is vital for any homeowner in financial distress. Both solutions help when you can’t keep up with mortgage payments, but they lead to different financial repercussions and timelines. The mortgage lender plays a crucial role in both situations, and knowing your path forward can make a world of difference. In the following sections, you’ll see how a short sale works, how it’s different from foreclosure, and what this could mean for your future.

Florida homeowners in cities like Orlando and Tampa are often surprised by how quickly a missed payment can lead to foreclosure. EPS Houses specializes in providing subject-to solutions that help homeowners in these areas stay in control of their property and avoid damaging their credit through a short sale. By working with experts who understand the local market and lender processes, you can explore options that keep you empowered, even in challenging times.

What Is a Short Sale in Real Estate?

A short sale happens when you sell your home for less than the remaining mortgage balance, but only after getting your mortgage lender’s approval. If your home’s current market value drops below what you owe, and you’re facing a genuine financial hardship, you can request this arrangement. The process begins by submitting proof of hardship and financial documents to your lender, along with a hardship letter describing your situation.

The lender then evaluates your request and compares the market value to the outstanding mortgage. If approved, you work with a real estate agent to list and sell your home, but the lender controls negotiations and must sign off on the final purchase price. Unlike foreclosure, a short sale is a voluntary step taken by the homeowner to avoid more severe consequences.

Can you explain what a short sale is in real estate and how it differs from foreclosure? A short sale is a proactive solution where you sell for less than the loan balance; foreclosure is when the lender forcibly takes the property due to missed mortgage payments.

To illustrate how homeowners can avoid foreclosure, consider the story of Maria, a Florida homeowner facing overwhelming financial difficulties. With mortgage payments piling up and the risk of foreclosure looming, Maria discovered a solution by selling her home subject-to to EPS Houses. Rather than undergoing the stressful foreclosure process, she worked with EPS Houses, who took over her existing mortgage payments and allowed her to move on without the damage of foreclosure on her record. By acting quickly, Maria preserved her credit and gained peace of mind, showing how alternative options to foreclosure—like selling subject-to—can make a life-changing difference.

Key Differences Between Short Sale and Foreclosure

Short sales and the foreclosure process both occur when mortgage payments can’t be met, but they are not the same. In a short sale, you work with your lender to sell your home and may avoid the harshest credit consequences. In contrast, foreclosure is a legal action where the lender seizes your property, often leading to greater credit damage and stress.

Here’s a comparison table to highlight the main differences:

| Aspect | Short Sale | Foreclosure |

|---|---|---|

| Initiated By | Homeowner (voluntary) | Lender (legal action) |

| Lender Approval | Required for sale price and terms | Lender takes possession |

| Effect on Credit Score | Moderate drop (usually less than foreclosure) | Significant, long-lasting damage |

| Control of Sale | Homeowner (with lender approval) | Lender sells, homeowner evicted |

| Deficiency Judgment | Possible, lender may forgive some debt | Possible, varies by state |

| Waiting Period for Loan | Shorter (typically 2 years) | Longer (up to 7 years) |

Can you explain what a short sale is in real estate and how it differs from foreclosure? This table clarifies their legal, financial, and emotional differences.

How Short Sales Impact Your Credit Score

If you complete a short sale, your credit score will take a hit, but not as severely as with a foreclosure. The actual impact depends on your credit history and the number of missed mortgage payments leading up to the short sale. Typically, a short sale can drop your score by 85–160 points, while foreclosure could mean a 200–300 point decrease.

- Short sales appear as “settled for less than owed” on your credit report.

- The higher your initial credit score, the bigger the potential drop from a short sale.

- Lenders may require a waiting period before you can qualify for a new mortgage, but it’s shorter than after a foreclosure.

What are the financial and credit consequences for homeowners who go through a short sale? Expect moderate credit damage, possible waiting periods for a new mortgage, and potential deficiency judgments if the lender doesn’t forgive the remaining debt.

Why Homeowners Face the Risk of Short Sales

Experiencing financial hardship isn’t rare, and many homeowners in the United States find themselves unable to keep up with mortgage payments when unexpected life events strike. Falling home values or tough market conditions can turn a manageable situation into a crisis, especially if you owe more than your house is worth. When loss mitigation options run out, a short sale may seem like the only path forward. Let’s look at common causes behind mortgage defaults and warning signs you might face a short sale.

Common Reasons for Mortgage Default in the U.S.

Mortgage default often results from financial hardship or a sudden change in your financial situation. Many homeowners fall behind for reasons such as:

- Loss of steady income due to job loss or reduced hours.

- Unexpected medical bills or major life expenses.

- Sharp declines in home values, leaving you owing more than your property is worth.

If you’re unable to resolve missed mortgage payments through loss mitigation, default can happen quickly. Other triggers include divorce, disability, or overwhelming debt that makes keeping up with the mortgage impossible. These circumstances force homeowners to seek alternatives like loan modification, forbearance, or creative financing such as subject-to real estate. Are there any alternatives to a short sale if a homeowner is struggling to pay their mortgage? Yes—loan modification, forbearance programs, deed in lieu, or subject-to sales can all provide options.

Signs You May Be Headed Toward a Short Sale

Spotting the red flags early can help you avoid foreclosure or a short sale. If you’re consistently struggling with mortgage payments, communicating with your lender and seeking help is critical. Warning signs include:

- Notices of default or legal action from your mortgage holder.

- Repeated late or missed mortgage payments, leading to mounting penalties.

- Letters from your lender about possible foreclosure sale dates.

If your outstanding mortgage keeps growing and selling your home wouldn’t cover the debt, you may be headed toward a short sale. Early action and exploring creative solutions like subject-to real estate can help you avoid the financial and emotional fallout. What are the main steps involved in the short sale process for both buyers and sellers? Early identification, lender negotiations, home listing, and closing are key stages.

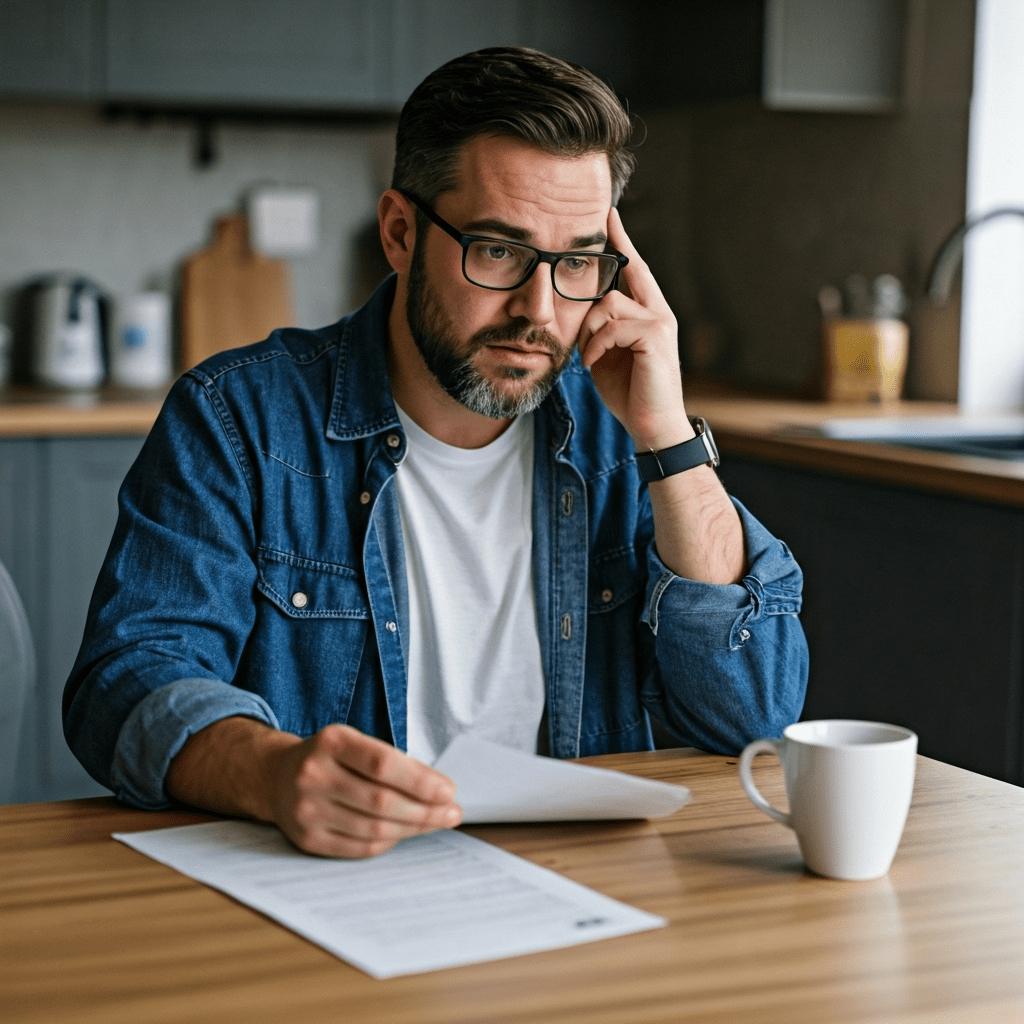

Financial and Emotional Consequences for Homeowners

Facing a short sale brings significant financial and emotional challenges. Not only does your credit score suffer, but you may also face a period of financial stress as you work through the mortgage lender’s requirements. The uncertainty and loss of your home can damage your sense of security.

The financial hardship includes potential deficiency judgments if the lender doesn’t forgive all remaining debt, making it even harder to recover financially. This process often brings stress, anxiety, and the feeling of losing control. Still, acting proactively and exploring alternatives, such as subject-to real estate transactions, can help minimize damage to your credit and emotional well-being. What are the financial and credit consequences for homeowners who go through a short sale? Credit damage, potential for lingering debt, and emotional distress.

Alternatives to Short Sales: What Are Your Options?

Before you commit to a short sale, it’s wise to review every available alternative. Your financial situation might allow for options that protect both your homeownership and your credit score. Loan modification, forbearance, deed in lieu of foreclosure, and creative financing like subject-to real estate deals each offer different benefits. The best option depends on your personal circumstances and the willingness of your mortgage lender. In the next sections, we’ll explore these alternatives and how they can help you.

Loan Modification and Forbearance Programs

Loan modification and forbearance programs are popular alternatives to short sale for homeowners in trouble. Loan modification involves permanently changing the terms of your mortgage, making payments more manageable by reducing interest rates, extending loan terms, or adjusting the principal. Forbearance, in contrast, lets you temporarily pause or reduce payments during a period of financial hardship.

- Loan modifications can help you stay in your home by making payments affordable.

- Forbearance is useful for short-term financial hardship but doesn’t eliminate the underlying debt.

- Both require cooperation with your mortgage lender and may involve loss mitigation counseling.

Are there any alternatives to a short sale if a homeowner is struggling to pay their mortgage? Loan modification and forbearance are key options that can reduce or delay payments, giving you time to recover financially.

Deed in Lieu of Foreclosure

A deed in lieu of foreclosure is another way to avoid the traditional foreclosure process. Here, you voluntarily transfer ownership of your home to the mortgage holder, and in return, your remaining balance may be forgiven. This option lets you walk away without the stress of a foreclosure sale.

However, it still leaves a mark on your credit and may not be available if there are other liens on the property. Some lenders may still pursue a deficiency judgment for any remaining debt, so legal advice is essential. This approach may help you avoid further legal action and could be less stressful than a drawn-out foreclosure, but it still means leaving your home behind. Are there any alternatives to a short sale if a homeowner is struggling to pay their mortgage? Deed in lieu is another option, though it doesn’t let you keep your property.

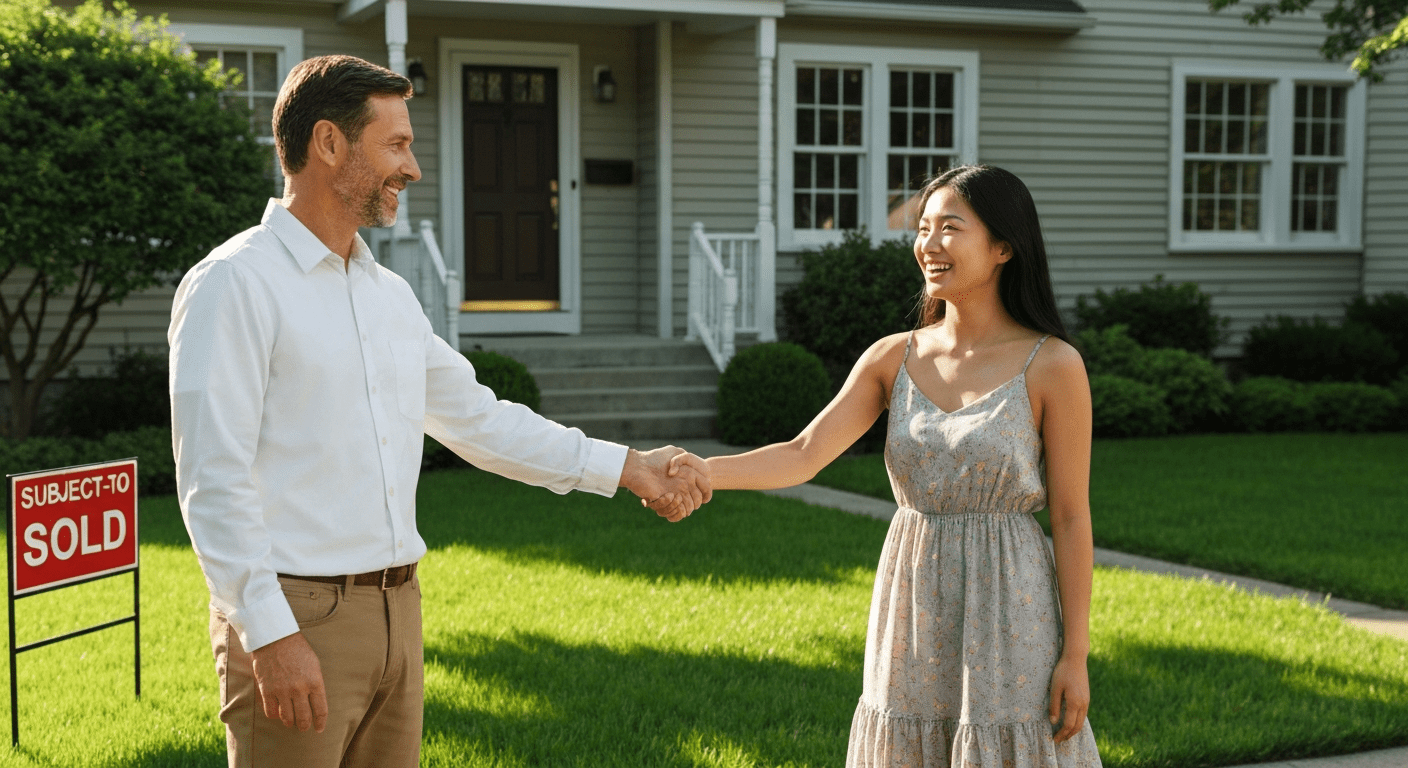

Selling Your Home “Subject-To” as a Solution

Subject-to real estate is a form of creative financing that can be a lifeline for distressed homeowners. In this scenario, you sell your home to a buyer who takes over the responsibility of making your mortgage payments, keeping the original mortgage in place.

- Subject-to real estate allows you to avoid the lengthy short sale process and stop foreclosure quickly.

- It can protect your credit by preventing a foreclosure or short sale from appearing on your record.

- EPS Houses specializes in helping homeowners in financial hardship sell their properties subject-to, offering a streamlined process and immediate relief.

Are there any alternatives to a short sale if a homeowner is struggling to pay their mortgage? Yes—subject-to deals like those offered by EPS Houses are a fast, effective way to avoid foreclosure and save your credit.

Introduction to “Subject-To” Real Estate Transactions

“Subject-to” real estate deals are a unique approach to creative financing, providing distressed homeowners with options that traditional sales can’t match. Instead of waiting for a lender’s approval or facing the stress of a foreclosure process, you can sell your home quickly while keeping the mortgage payments current. Real estate agents and companies like EPS Houses help facilitate these transactions, allowing you to move on without wrecking your credit or facing a lengthy approval process. Now, let’s break down how “subject-to” transactions work.

What Does “Subject-To” Mean in Real Estate?

In real estate, a “subject-to” transaction means the buyer acquires your home “subject to” the existing mortgage. Instead of paying off the outstanding mortgage at closing, the buyer agrees to continue making your mortgage payments. This creative financing method allows the home sale to proceed even if you have little or no equity, and it eliminates the need for traditional lender approval.

The purchase price and terms are negotiated directly between you and the buyer, often with the help of a real estate agent experienced in subject-to deals. Because the mortgage remains in your name, the transaction can be completed quickly—sometimes within days. How does a homeowner qualify for a short sale, and what documentation is typically required? For a subject-to sale, you’ll need to provide proof of your mortgage balance and current financial hardship.

How “Subject-To” Sales Work for Distressed Homeowners

If you’re a distressed homeowner, a subject-to sale offers immediate relief from the burden of mortgage payments. Here’s how the process works:

- You work with a company like EPS Houses or a creative real estate agent to find a qualified buyer willing to take over your mortgage payments.

- The buyer makes payments directly to your lender, keeping your mortgage current and stopping the foreclosure process.

- You avoid the negative credit impact of both a short sale and foreclosure, giving you a chance to recover financially.

Financial hardship doesn’t have to end in foreclosure. Subject-to real estate transactions let you move on quickly without waiting for lender approval or damaging your credit. How fast can I sell my home “subject-to” compared to a short sale? Subject-to sales are often much faster—sometimes closing within days.

Comparing “Subject-To” Deals to Short Sales

Comparing subject-to deals with short sales reveals key differences in speed, credit impact, and control. Here’s what sets them apart:

- Subject-to real estate transactions are typically much quicker than the short sale process, which can drag on for months.

- With a subject-to sale, your credit score is protected because the mortgage stays current, while a short sale still damages your credit.

- Short sales require lengthy negotiations and lender approval, while subject-to deals let you set the sales price and terms directly.

Create a comparison blog between short sales and subject-to deals. Explain the pros and cons of each, and conclude why selling subject-to with EPS Houses is a better long-term option. In summary, subject-to sales provide faster solutions, more control, and greater protection for your credit—making them an ideal choice for many homeowners.

Beginner’s Guide: How to Sell Your Home “Subject-To”

Selling your home subject-to can be the quickest way to stop foreclosure and protect your credit score. The process is straightforward but requires due diligence and preparation. To get started, you’ll need the right documents, a clear understanding of your equity situation, and solid legal advice to ensure your interests are protected. This guide walks you through every step, so you can confidently sell your house before foreclosure and move forward with peace of mind.

What You Need to Get Started (Documents, Equity, Legal Advice)

A successful transition from homeownership requires careful preparation. Gathering essential documents like bank statements, hardship letters, and the current mortgage balance is crucial. Adequate equity in your property plays a significant role, ensuring that the sale proceeds can cover outstanding debts while avoiding a short sale scenario. Additionally, seeking legal advice from professionals familiar with the housing market can protect your interests and provide clarity on the sale process. This groundwork is vital in navigating financial stress while safeguarding your credit score.

Step-by-Step Guide to the “Subject-To” Sale Process

Selling your home subject-to follows a clear set of steps:

- Assess your financial situation and gather necessary documents.

- Find a qualified buyer, like EPS Houses, willing to take on your mortgage payments.

- Negotiate the sales price, terms, and responsibilities for making payments.

You’ll also want to consult a real estate attorney to draft the agreement and ensure compliance with state laws. What are the main steps involved in the short sale process for both buyers and sellers? The process involves documentation, buyer selection, negotiation, and closing—much like a short sale, but typically much faster and simpler.

Step-by-Step: Selling Your Home “Subject-To” Explained

The subject-to real estate sale process is designed to be straightforward, providing creative financing solutions while protecting your credit. Each step, from assessing your home’s market value to finalizing the deal, helps you avoid foreclosure and move on with your life. In the next sections, we’ll break down each stage so you know exactly what to expect and how to make sure your sale is successful from start to finish.

Step 1: Assess Your Financial Situation and Property Value

The first step in a subject-to sale is understanding your financial position and your home’s current market value. Gather your bank statements, mortgage balance, and details about your monthly mortgage payments. You’ll also want to know if your home is worth more or less than the outstanding mortgage.

A real estate agent or professional experienced in creative financing can help you determine your home’s fair market value using local sales data and the multiple listing service. Due diligence here ensures you have a realistic view of your options and that you’re setting yourself up for a successful sale. What is the first step in the “subject-to” sale process? Assess your finances, outstanding mortgage, and current market value.

Step 2: Find a Qualified “Subject-To” Buyer (Like EPS Houses)

Identifying a qualified “subject-to” buyer can significantly ease your financial pressures. Focus on individuals or entities experienced in creative financing, as they are more likely to understand the complexities of assuming mortgage payments without lender intervention. Utilizing a real estate agent familiar with the subject-to method can be invaluable. Ensure potential buyers conduct due diligence, including a home inspection, to assess the property’s condition and existing mortgage balance. This thorough approach helps secure a smooth transition, preventing further financial troubles and potential credit damage.

Step 3: Review and Negotiate the “Subject-To” Agreement

With a buyer lined up, you’ll move into the negotiation phase. Review the purchase price, the monthly payment schedule, and responsibilities for property taxes and insurance. The buyer should provide an approval letter or written commitment to continue making your mortgage payments.

Engage an attorney or real estate professional for legal advice to ensure the subject-to agreement covers all necessary details and protects your interests. Negotiation is your chance to address concerns and clarify all terms before moving forward. How do real estate agents and attorneys assist in the short sale process? They help negotiate favorable terms and safeguard your rights in the sale.

Step 4: Complete Legal and Title Requirements

Once terms are agreed upon, you’ll need to finalize legal and title requirements. A title company will verify the property’s legal status, check for any liens, and ensure the transfer is completed properly.

- All documents must be reviewed to avoid future legal action or disputes.

- A real estate attorney or title company representative will oversee the closing and ensure compliance with state laws.

- Due diligence during this phase is critical to protecting everyone involved.

How do real estate agents and attorneys assist in the short sale process? They ensure all legal and title work is completed accurately, preventing post-sale complications.

Step 5: Close the Deal and Protect Your Credit

The final step is closing the sale. At this point, the buyer assumes responsibility for making your mortgage payments, and you transfer ownership of your home.

- The title company or attorney will handle the sale proceeds and finalize all paperwork.

- Your credit score is protected because your mortgage stays current and foreclosure is avoided.

- Confirm with your lender that payments are being made as agreed and monitor your account for any issues.

Will selling my home “subject-to” stop foreclosure from appearing on my credit? Yes, as long as the mortgage stays current, foreclosure is avoided, and your credit remains intact.

Conclusion

In conclusion, navigating the complexities of short sales and foreclosures can be daunting, but selling your home “subject-to” offers a viable alternative to protect your credit. This method allows distressed homeowners to avoid the long-term repercussions of a short sale while still facilitating a successful transaction. By understanding the process and preparing effectively, you can safeguard your financial future and maintain your peace of mind. Knowledge is power, and with the right guidance, you can turn a challenging situation into a strategic opportunity. If you’re ready to explore this option further, get in touch with EPS Houses today for expert advice and support tailored to your circumstances.

Frequently Asked Questions

Will selling my home “subject-to” stop foreclosure from appearing on my credit?

Yes, selling your home subject-to real estate prevents foreclosure from appearing on your credit as long as your mortgage payments remain current. This approach stops the foreclosure process and protects your credit score, giving you a chance to recover financially and move forward.

Are there risks involved in “subject-to” sales for sellers?

While subject-to real estate offers many benefits, there are risks if the buyer fails to keep up with the outstanding mortgage payments. Always conduct due diligence, seek legal advice, and work with reputable professionals to minimize risk and ensure the creative financing arrangement is safe.

How fast can I sell my home “subject-to” compared to a short sale?

Subject-to sales are usually much faster than the short sale process. While short sales can take months due to lender involvement, selling subject-to with EPS Houses can be completed in days or weeks, allowing you to avoid foreclosure and complete the sale of the property much quicker.

Can I stay in my home after a “subject-to” sale?

Yes, you can often stay in your home after a “subject-to” sale. The buyer takes over the mortgage payments while you maintain possession. However, it’s crucial to establish clear terms in your agreement to avoid potential conflicts regarding occupancy and property management.