Key Highlights

Here’s a quick look at what we’ll cover to help you understand subject to real estate in Florida:

- Selling subject-to is a creative financing option where a buyer takes over your existing mortgage payments.

- The original mortgage remains in your name, which can pose a risk to your seller’s credit.

- A major risk is the “due-on-sale” clause, which allows the lender to demand full payment.

- Protecting your credit score involves vetting the buyer and creating a solid legal agreement.

- Proper due diligence is crucial to avoid credit damage from missed payments by the new buyer.

Introduction

Are you thinking about selling your home in Florida but worried about the traditional real estate process? Maybe you need to sell your house fast or are looking for a more flexible solution. Subject-to real estate in Florida offers a unique path. This type of creative financing allows a buyer to take over your mortgage payments, which can speed up the sale. However, it’s essential to understand how to protect your credit in this kind of deal. Let’s explore how you can sell subject-to without risking your financial standing.

Understanding Subject-To Real Estate in Florida

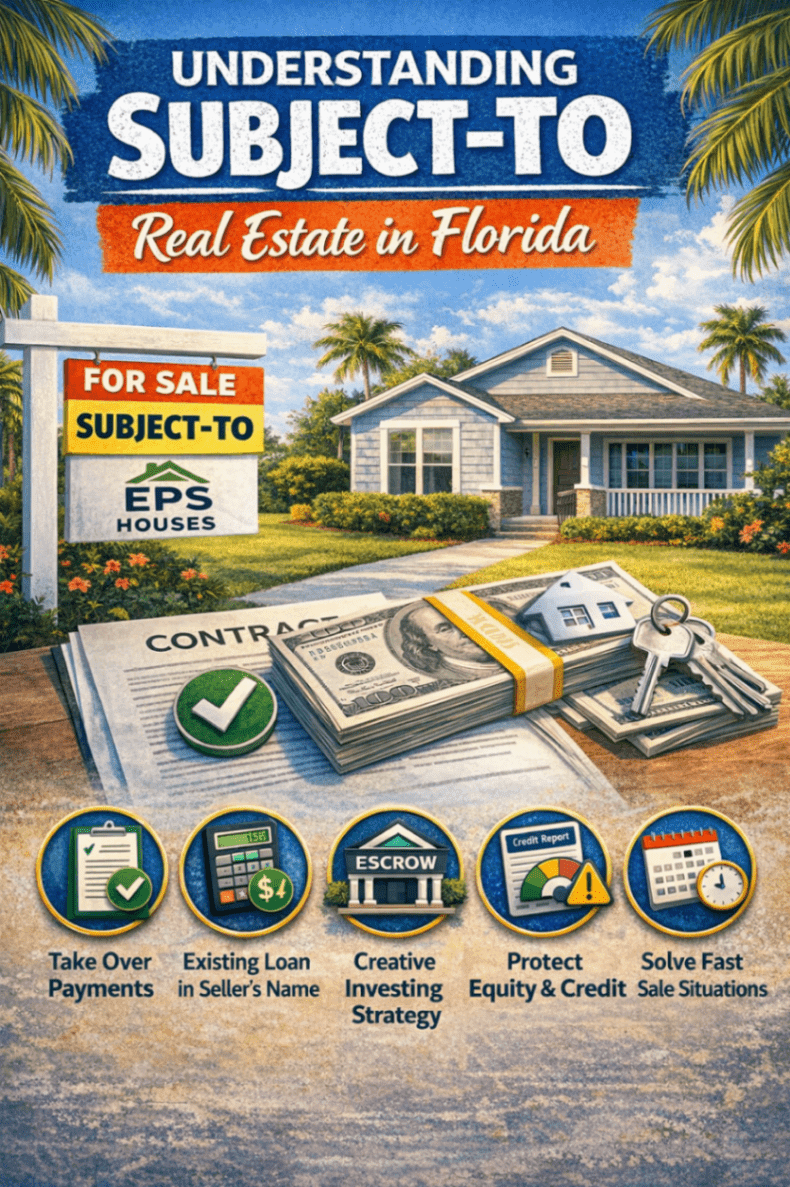

Selling your property through a subject-to real estate transaction in Florida means the buyer agrees to take over your mortgage payments. The key detail is that the existing mortgage stays in your name, even though the buyer now holds the property title.

This arrangement can be an excellent solution for sellers in difficult situations, but it comes with potential risks. One of the biggest concerns is the “due-on-sale” clause in your mortgage, which we’ll discuss in more detail. Let’s look closer at what “subject-to” means and how these deals work in the Sunshine State.

What Does “Subject-To” Mean in Real Estate Deals?

In the simplest terms, “subject-to” means the buyer is purchasing your property “subject to” the existing mortgage. This is a form of creative financing where the buyer doesn’t get a new loan. Instead, they agree to make the monthly payments on your current home loan.

The most important thing for you to understand is that the existing mortgage remains in the seller’s name. Even though you’ve sold the property and the deed is transferred to the buyer, you are still legally responsible for the debt in the eyes of the lender.

This is very different from a traditional sale where the buyer gets their own financing, and your mortgage is paid off at closing. With a subject-to deal, your name stays on the loan until the buyer either pays it off or refinances it into their own name. This is why protecting your credit is so important.

How Does a Subject-To Transaction Work in Florida?

A subject-to transaction in Florida begins when you and a buyer agree on the terms. The new buyer agrees to take over your mortgage payments. You will then sign a purchase agreement that clearly outlines this arrangement. It’s highly recommended to have a real estate attorney draft or review this document to protect your interests.

Once the agreement is signed, the property title is transferred to the buyer at closing. However, the existing mortgage loan isn’t paid off. It remains in your name, and you are still ultimately responsible for it. This is a critical point that can affect your seller’s credit if the buyer misses a payment.

The new buyer will then start making the mortgage payments directly to the lender. For you, the seller, this means you must have a system in place to verify that payments are being made on time every month. This ongoing responsibility is the biggest difference compared to a traditional sale.

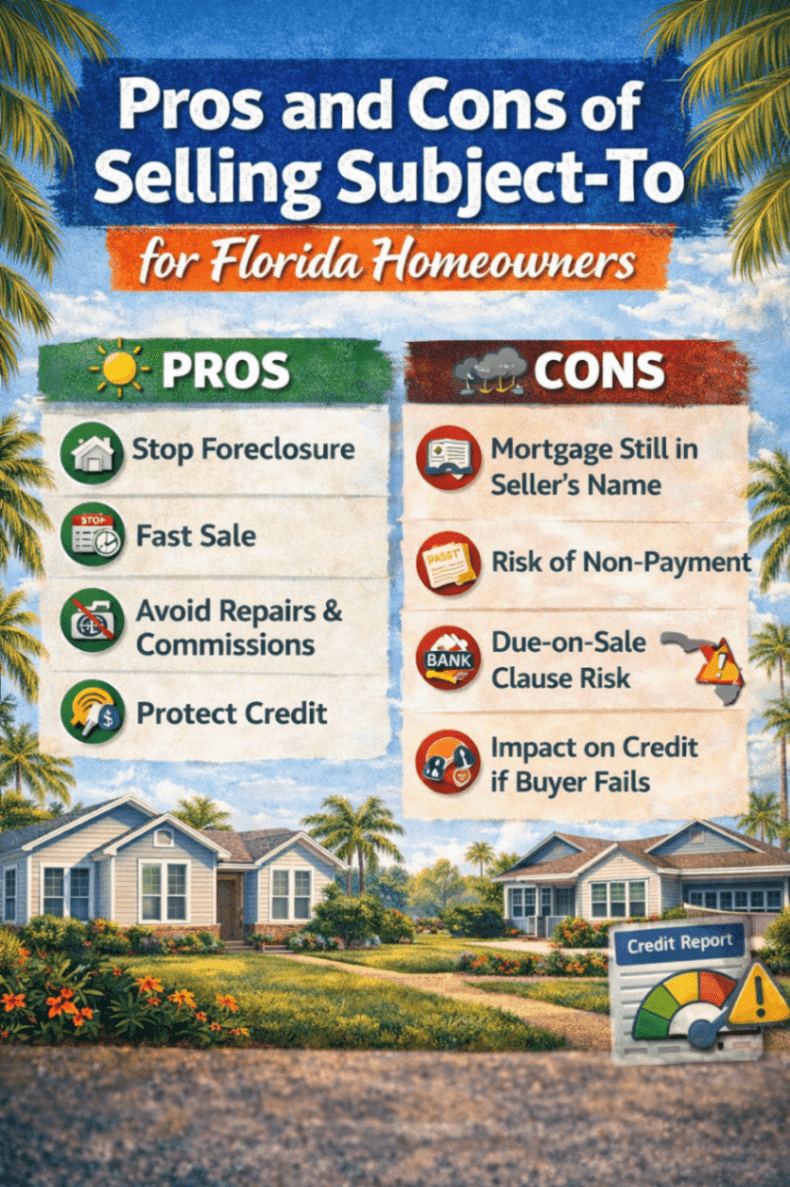

Pros and Cons of Selling Subject-To for Florida Homeowners

Opting for a subject-to deal in Florida can be a game-changer, especially if you need to sell your house fast. This approach can help you avoid foreclosure and get out from under a mortgage quickly. However, it’s not without its drawbacks.

The main concern for sellers is the potential risks to their credit. Since the mortgage stays in your name, any late or missed payments by the buyer will directly impact your seller’s credit score. We’ll examine both the bright side and the potential pitfalls of this strategy.

Benefits of Subject-To Transactions for Sellers

One of the biggest advantages of selling your home with this creative financing method is the speed of the transaction. A subject-to sale bypasses the lengthy process of a buyer needing to secure a new loan. This means you can achieve a quick sale, often closing in a matter of days instead of weeks or months.

This is especially helpful if you’re facing financial distress, such as foreclosure. A fast sale can stop the foreclosure process and provide immediate relief. It also helps you get out of a property that might be hard to sell traditionally, perhaps because it needs repairs you can’t afford. You can often sell as-is.

Here are some key benefits:

- Quick Sale: Close the deal much faster than a traditional sale since there is no bank needed for the buyer.

- Avoid Foreclosure: A subject-to sale can be a lifeline if you are behind on payments, helping you avoid serious credit damage.

- Get Payments Covered: You can move on without worrying about the monthly mortgage payment, as the buyer takes over.

- Sell an “Unsellable” Home: This is a great option for properties that need repairs or have little equity.

Potential Risks for Sellers, Especially Credit Concerns

The primary risk in a subject-to real estate transaction revolves around your credit. Because the mortgage remains in your name, you are still on the hook with the lender. If the buyer you sell to misses a payment, it’s your credit score that will take a hit.

This can lead to significant credit damage, making it difficult for you to get a new loan for a car or another home in the future. Your debt-to-income ratio will also reflect the existing mortgage, which can be a barrier to future financing until the loan is paid off.

Here are the main credit-related risks:

- Late Payments: If the buyer pays late, it will be reported on your credit report.

- Default: In a worst-case scenario, if the buyer stops paying altogether, the lender will start foreclosure proceedings against you.

- Debt-to-Income Ratio: The mortgage debt stays on your credit profile, which can prevent you from qualifying for new loans.

- Due-on-Sale Clause: The lender could demand the full repayment of the loan if they discover the title transfer.

Protecting Your Credit in a Subject-To Sale

Given the risks involved, protecting your seller’s credit must be your top priority in any subject to real estate Florida deal. You can’t just hand over the keys and hope for the best. You need to take proactive steps to ensure the mortgage is paid on time.

Successfully navigating a subject-to sale means putting safeguards in place from the very beginning. From vetting the buyer to structuring the agreement correctly, every step is crucial for maintaining your credit score. Let’s look at the specific actions you can take and the mistakes you must avoid.

Steps to Keep Your Credit Secure During the Process

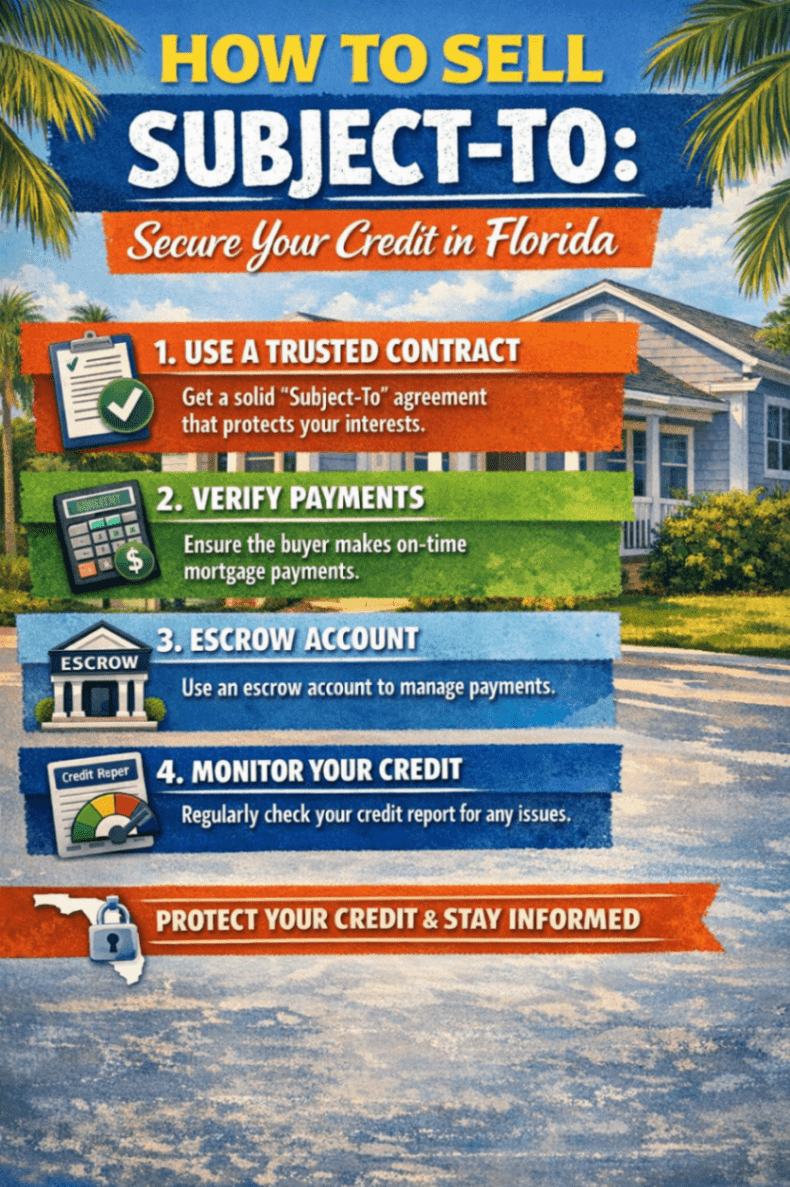

To protect your credit score, your first step is thorough due diligence on the buyer. Don’t just take their word that they can make the payments. You need to verify their financial stability and their track record with paying bills on time.

Work with an experienced real estate attorney to draft a strong contract. This agreement should include clauses that protect you. For example, it could require the buyer to refinance the loan within a certain period or give you the right to take back the property if they miss payments.

Here are essential steps to secure your credit:

- Vet the Buyer: Ask for proof of income, check their credit, and look at their payment history. A reliable cash home buyer like EPS Houses has a proven track record.

- Use a Solid Contract: Hire a real estate attorney to create an agreement that outlines the buyer’s responsibilities and the consequences of default.

- Set Up Payment Verification: Arrange for a third-party servicing company to collect payments or get online access to the loan account to monitor the payment history yourself.

- Require Insurance: Make sure the buyer maintains homeowner’s insurance on the property and lists you as an additional insured party.

Common Credit Mistakes to Avoid as a Seller

One of the biggest mistakes sellers make is failing to properly vet the buyer. It’s easy to be swayed by a quick offer, especially if you’re in a tough spot. However, selling to an unreliable buyer almost guarantees future problems and credit damage. Always put in the effort to check their financial background.

Another common error is not having a robust legal agreement in place. A simple handshake deal or a poorly written contract leaves you exposed. Without clear terms, you have little recourse if the buyer fails to make timely payments on the mortgage payments.

Avoid these common mistakes to protect your seller’s credit:

- Not Vetting the Buyer: Never sell to someone without verifying their ability and willingness to pay.

- Using a Weak Contract: A poorly drafted agreement won’t protect you if things go wrong.

- Failing to Monitor Payments: Don’t assume the buyer is making payments. You must track the payment history yourself.

- Ignoring the Due-on-Sale Clause: Be aware that the lender could call the loan due and have a contingency plan in place.

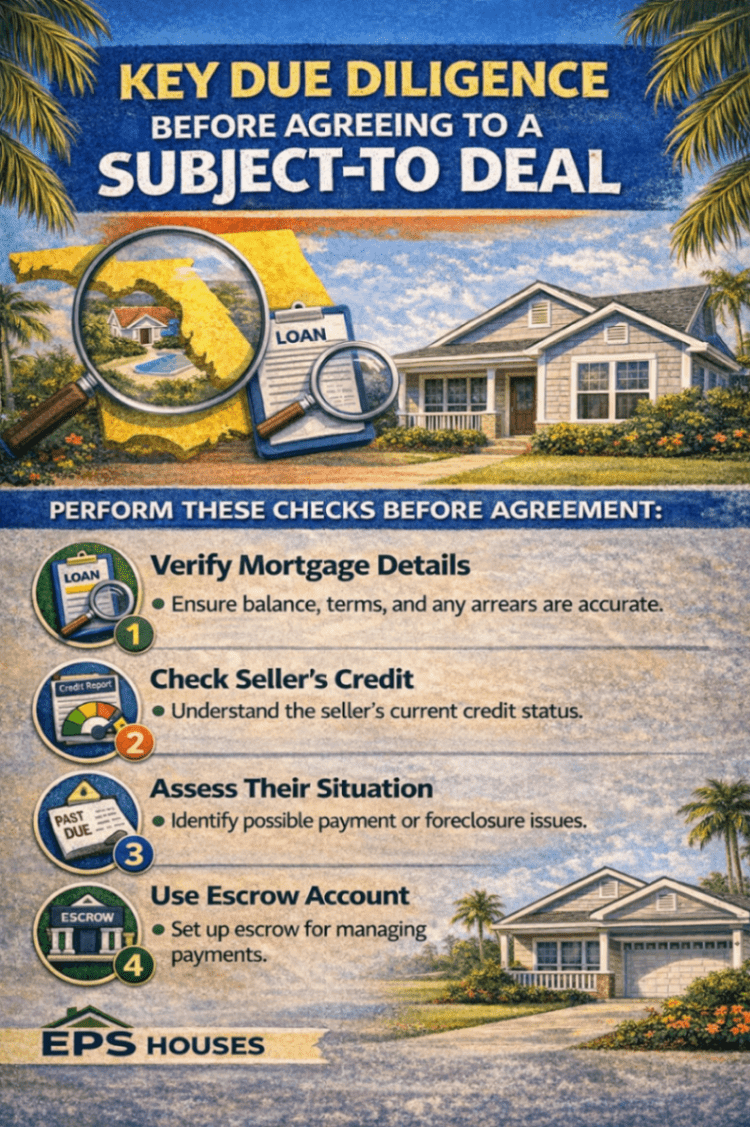

Key Due Diligence Before Agreeing to a Subject-To Deal

Before you sign any papers for a subject to real estate Florida deal, completing your due diligence is non-negotiable. This is the research you do to ensure you’re making a safe and informed decision. It involves looking into the buyer’s background and carefully reviewing your mortgage and property title.

Working with professionals like a real estate attorney and a title company can help you uncover any potential issues before they become major problems. Let’s break down the two main areas you need to investigate: the buyer’s qualifications and your title and mortgage documents.

Reviewing Buyer Qualifications and Payment History

When you sell your house subject-to, you are essentially acting as the bank. You need to be just as careful as a lender would be. The most important part of your due diligence is thoroughly vetting the potential buyer, especially if they are a real estate investor you don’t know.

Start by asking for documentation that proves their financial stability. This can include bank statements, pay stubs, and tax returns. A serious buyer will understand why you need this information. You can also run a credit check to see their payment history and how they’ve managed debt in the past.

Look for a buyer with a strong track record. An established real estate investor or company like EPS Houses, with a history of successful subject-to deals, is often a safer bet than an individual doing this for the first time. Their reputation depends on making payments, which protects your seller’s credit.

Important Title and Mortgage Considerations

Beyond the buyer, you need to review your own documents with a fine-tooth comb. Start with your mortgage agreement. You must find and understand the “due-on-sale” clause, also known as an acceleration clause. This provision gives your lender the right to demand full repayment of the loan if you transfer the title without their permission. A real estate attorney can help you understand the specific risks here.

Next, you’ll need to work with a title company to run a title search. This will confirm that you have a clear title to the property and reveal any liens or judgments that need to be addressed before the sale. A clean title is essential for a smooth transaction.

Here are key items to check:

| Consideration | Why It Matters for Your Credit |

|---|---|

| Due-on-Sale Clause | If the lender triggers this, you could face immediate demand for the full loan balance, leading to foreclosure if unpaid. |

| Existing Liens | Any liens on the title (like from a contractor or the IRS) must be cleared, or they could complicate the sale and your finances. |

| Loan Type | Some loans, like FHA or VA loans, have stricter rules about transfers and assumptions that you need to be aware of. |

| Escrow Account | Understand how property taxes and insurance will be paid from escrow after the buyer takes over mortgage payments. |

Best Practices for Reducing Credit Risk When Selling Subject-To

When you decide to move forward with a subject to real estate Florida sale, your goal is to minimize your credit risk as much as possible. This involves being proactive and strategic in how you structure the deal and how you manage it after the closing.

By implementing some best practices, you can create a safety net that protects you if the buyer runs into trouble. Let’s discuss how to structure your agreement for maximum protection and how to effectively monitor the ongoing mortgage payments to catch any issues early.

Structuring Agreements to Minimize Exposure

The best way to reduce your risk is to have a comprehensive and detailed legal agreement. This is not a time for a standard, one-page contract. You need a document created by a real estate attorney that is specifically designed for a subject-to transaction and its unique legal implications.

Your agreement should clearly state the consequences if the buyer defaults. For example, you can include a “performance mortgage” or a “deed in lieu of foreclosure” clause. This gives you the legal right to take back the property quickly if the buyer fails to uphold their end of the deal, without having to go through a lengthy court process.

Here are ways to structure your agreement to reduce risk:

- Include a Performance Deed: Have the buyer sign a deed that transfers the property back to you, which is held by an attorney and only recorded if they default.

- Require a Refinance Deadline: Add a clause that requires the buyer to refinance the property into their own name within a set timeframe, such as 3-5 years.

- Specify Late Fees: Outline clear penalties for late payments that the buyer must pay to you directly. This incentivizes them to pay on time.

- Owner Financing for Equity: If you have equity, you can create a second loan (a form of seller financing) that gives you more legal standing if problems arise.

Monitoring Ongoing Mortgage Payments

Your job isn’t over once the closing is complete. Ongoing monitoring of the mortgage payments is essential to protect your credit. Never assume the buyer is making timely payments; you must verify it every single month.

One of the easiest ways to do this is to retain online access to your mortgage account. You can log in each month to confirm the payment has been made. Alternatively, you can arrange for the lender to send you monthly statements or notifications. Some sellers and buyers agree to use a third-party loan servicing company, which collects payments from the buyer and pays the lender, providing a clear record for both parties.

Here are effective ways to monitor payments:

- Retain Online Account Access: Log in to the lender’s portal monthly to see the payment history.

- Use a Third-Party Servicer: Hire a company to manage the payments, which adds a professional layer of oversight.

- Set Up Alerts: Ask your lender if you can receive email or text alerts when a payment is made or if it becomes past due.

- Check Your Credit Report: Regularly review your credit report to ensure the mortgage is being reported as “paid as agreed.”

Frequently Asked Questions (FAQ)

Understanding the intricacies of selling subject-to can lead to many questions. Common inquiries often revolve around the potential risks involved, including how existing mortgage terms affect the seller’s credit score and cash flow. Legal implications may arise in such transactions, making it crucial to consult with a real estate attorney. Questions about navigating the sale process, ensuring a smooth transfer of the seller’s name, or the viability of new financing options also frequently emerge. Clear communication is key to addressing these concerns.

How Can I Sell Subject-To Without Impacting My Credit Score?

To sell subject-to without impacting your credit score, you must ensure the buyer makes all mortgage payments on time. This involves thoroughly vetting the buyer’s financial stability, using a strong legal agreement drafted by an attorney, and actively monitoring the account each month to confirm timely payments are made.

Will a Subject-To Sale Show Up on My Credit Report?

The subject-to sale itself does not appear on your credit report. However, the existing mortgage loan will continue to show up on your credit report because it remains in your name. Each monthly payment the buyer makes will be reported, positively impacting your credit as long as it’s on time.

Is It Safe to Sell My House Subject-To Without Paying Off the Mortgage First?

It can be safe, but it carries inherent risks. The main risk is that the mortgage stays in your name, making you responsible for payments if the buyer defaults. To make it safer, you need to perform thorough due diligence on the buyer and have a real estate attorney create a protective contract.

Conclusion

In conclusion, selling subject-to in Florida can be a powerful strategy when approached correctly. Understanding the ins and outs of this method not only helps you leverage your property effectively but also safeguards your credit. By remaining mindful of potential risks and implementing best practices, you can navigate the process confidently. Remember, due diligence is key—ensuring buyer qualifications and structuring agreements wisely will minimize exposure to credit risk. If you’re considering a subject-to sale, don’t hesitate to get in touch for a suitability review and expert guidance on the steps to take. Your path to a successful transaction awaits!