How to stop Foreclosure

Key Highlights

- You can stop the foreclosure process by working with your lender on a loan modification to make payments more affordable.

- Filing for bankruptcy provides an automatic stay, which temporarily halts the foreclosure proceedings and gives you breathing room.

- If you have missed payments, a short sale or a deed-in-lieu of foreclosure allows you to give up the property and avoid foreclosure.

- Seeking legal help from a HUD-approved housing counselor or an attorney is crucial for effective foreclosure prevention.

- You can sell the house before foreclosure to a cash home buyer for a fast and simple solution.

Introduction

Facing foreclosure in Florida can feel overwhelming, but you have options. Understanding the foreclosure process and Florida’s foreclosure laws is the first step toward protecting your home and your financial future. As Florida homeowners, you have rights and several paths you can take to stop foreclosure. This guide provides a clear action plan for 2025, helping you navigate your choices, from negotiating with your lender to exploring a quick sale of your property.

Understanding Foreclosure in Florida: What’s Happening in 2025

In Florida, foreclosure is a judicial process, which means the lender must go through the court system to take your home. This process has specific steps and deadlines according to Florida law, giving you time to respond and defend your property.

Understanding these foreclosure proceedings is critical. Missing a deadline could result in a foreclosure sale, so it’s important to act fast. A housing counselor can help you understand the timeline and your options. Let’s look at how the process works and what rights you have.

How the Florida Foreclosure Process Works and Key Deadlines

Foreclosure Timeline

The foreclosure process in Florida begins after you miss several mortgage payments. Your lender will send you legal notices before filing a lawsuit. Once the lawsuit is filed, you will be served with a summons and have 20 days to file a formal response with the court.

Ignoring these notices can lead to a default judgment, allowing the lender to schedule a foreclosure sale. It is crucial to respond within the deadline to protect your rights. Florida foreclosure laws require the lender to follow these steps, giving you an opportunity to challenge the foreclosure proceedings.

Here is a simple breakdown of the timeline:

Stage | Key Action | Your Deadline |

|---|---|---|

Pre-Foreclosure | Lender sends a breach letter. | Typically 30 days to cure the default. |

Lawsuit Filed | Lender files a lawsuit and serves you. | 20 days to respond after being served. |

Judgment | Court reviews the case and may issue a judgment. | Varies based on court schedule. |

Foreclosure Sale | The property is scheduled for a public auction. | Usually 20-35 days after judgment. |

Your Rights and Protections as a Florida Homeowner

As a Florida homeowner, you have specific mortgage rights designed to protect you. First, your lender must prove they have the legal standing to foreclose. This means they must produce the original promissory note. If they can’t, you may have a valid defense.

You also have the right to challenge the foreclosure in court. This is where seeking legal help becomes essential. An attorney can review your loan documents for errors or violations of foreclosure laws. Many Florida homeowners find success by actively participating in their defense.

Furthermore, you have the right to pursue loss mitigation options at any point before the foreclosure sale. This includes applying for a loan modification, a short sale, or a deed-in-lieu of foreclosure. Knowing your rights empowers you to take control of the situation and find the best solution.

Common Reasons Homeowners Face Foreclosure in Florida

Many homeowners face foreclosure due to unexpected financial hardship. The most common reason is falling behind on missed payments, which can quickly spiral into overwhelming mortgage debt. A sudden change in your financial situation can make it impossible to keep up.

Events like job loss, a medical emergency, or divorce can disrupt your ability to pay your mortgage. Understanding these common triggers can help you see that you are not alone in this struggle. Below, we’ll explore these reasons in more detail.

Missed Mortgage Payments and Financial Hardship

The journey toward foreclosure almost always starts with missed payments. A temporary financial hardship, like an unexpected car repair or a reduction in work hours, can cause you to fall behind on your monthly payments.

When this happens, lenders begin adding late fees and other charges, making it even harder to catch up. A difficult financial situation that lasts for a few months can quickly put you at risk of foreclosure, as the amount you owe grows larger.

The key is to address the issue as soon as you realize you might miss a payment. Contacting your lender early can open up options that might not be available later. Acknowledging the financial hardship and seeking a solution is a proactive step toward avoiding foreclosure.

Effects of Unemployment, Medical Bills, and Divorce

Life-altering events are often the root cause of financial difficulties. Sudden unemployment can eliminate your primary source of income, making it impossible to cover your mortgage. This is one of the most common reasons homeowners fall into foreclosure.

Similarly, unexpected medical bills can drain your savings and disrupt your budget, forcing you to choose between paying for healthcare and your home. Divorce can also strain your financial situation, as it often involves splitting assets and managing two separate households on incomes that once supported one.

During these difficult financial times, it is important to know that help is available. These situations are often temporary, and there are programs and strategies designed to help you navigate them without losing your home.

Documents and Information Needed to Act Fast

To stop foreclosure, you need to be organized and act quickly. Gathering all your important paperwork is the first step. This includes your mortgage loan documents, recent financial statements, and any foreclosure notices you have received.

Having these documents ready will make it easier to negotiate with your lender or seek legal advice. Your current mortgage statement contains key information about your loan servicer and the amount you owe. We will explore what to gather and who to contact next.

Gathering Mortgage Records, Financial Statements, and Legal Notices

When you’re facing foreclosure, having your documents in order is essential for any negotiation or legal action. Start by finding all paperwork related to your mortgage loan. This includes the original agreement, which details the terms of your loan.

You will also need to assemble your recent financial statements. This shows the lender your current income, expenses, and overall financial picture. These documents are necessary when applying for assistance or a loan modification.

Finally, keep all legal notices and correspondence from your lender in one place. These documents contain critical deadlines and contact information. Here is a quick checklist:

- Mortgage statements and original loan documents

- Recent pay stubs, tax returns, and bank statements

- All foreclosure notices or letters from your lender

Setting Up Communication With Lenders and Legal Help

Open communication is your best tool for stopping foreclosure. Your first call should be to your mortgage servicer, the company that collects your payments. Be honest about your financial situation and ask what options are available to you.

At the same time, you should seek professional legal help. A HUD-approved housing counselor can provide free guidance and help you negotiate with your lender. These counselors are trained to help homeowners find solutions.

If your case is complex, an attorney can offer expert advice. You can also file a complaint with the Attorney General’s Office if you believe your lender is acting unfairly. Here’s who to contact:

- Your mortgage servicer (phone number is on your statement)

- A HUD-approved housing counselor

- A foreclosure defense attorney for legal advice

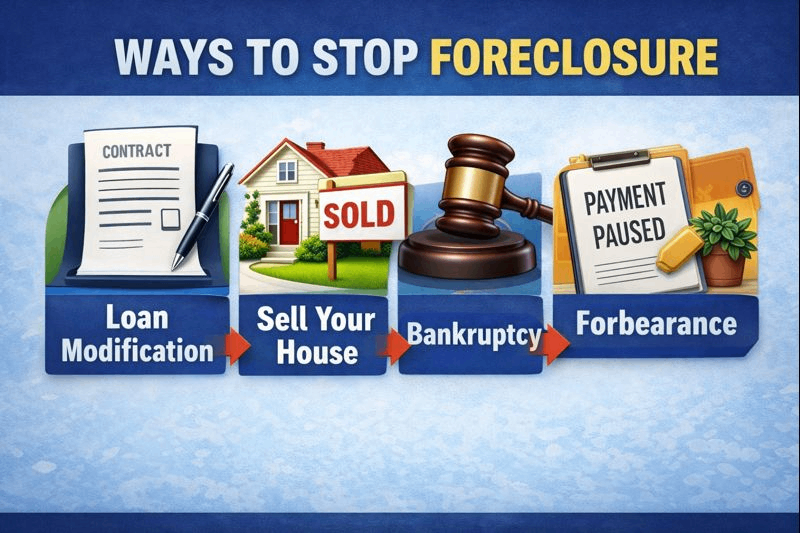

Immediate Actions That Can Help Stop Foreclosure

Ways to stop foreclosure

If you are facing imminent foreclosure, you need to take immediate action. Fortunately, there are several effective strategies you can use. Exploring a loan modification or a repayment plan with your lender is often the best first step.

These options can make your mortgage more affordable and help you get back on track. In other cases, you may need to consider legal advice for foreclosure defense or filing for bankruptcy. Let’s look at these powerful solutions more closely.

Contacting Your Lender and Exploring Loan Modification

One of the most effective foreclosure prevention tools is a loan modification. This is a permanent change to your loan terms designed to make your payments more manageable. You can negotiate directly with your lender to achieve this.

When you contact your lender, explain your financial situation and ask about their modification programs. They may offer to lower your interest rate or extend the loan term. Another option is a repayment plan, which lets you catch up on missed payments over a set period.

To apply, you will typically need to provide:

- A hardship letter explaining your circumstances

- Proof of income, like pay stubs

- Recent bank statements and tax returns

Acting quickly gives you the best chance of getting approved and stopping foreclosure.

Filing for Bankruptcy or Requesting Mediation

Filing for bankruptcy is a powerful legal tool that provides immediate, temporary relief from foreclosure. The moment you file, an “automatic stay” goes into effect. This court order stops your lender from continuing with foreclosure proceedings.

A bankruptcy attorney can help you decide which form of bankruptcy is right for you. Chapter 13 is often preferred for homeowners, as it allows you to create a repayment plan to catch up on missed payments over three to five years.

Chapter 7, on the other hand, liquidates assets to pay off unsecured debts and provides only a brief pause in the foreclosure.

- Chapter 13: Creates a payment plan to catch up on your mortgage.

- Chapter 7: Offers short-term relief but may not save your home long-term.

- Automatic Stay: Immediately stops all collection activities, including foreclosure.

Selling Your Home Quickly: Creative Solutions for Florida Homeowners

Sell Before Auction

Selling your home can be a quick and stress-free process, especially for Florida homeowners facing financial challenges. Consider options like selling as-is to a cash home buyer or exploring seller financing, which allows you to offer owner financing. Creative financing solutions, such as lease options or no bank needed sales, can attract qualified buyers. These methods help you sell your house fast, giving you a chance to regain financial stability while avoiding the lengthy foreclosure process.

Working With EPS Houses, a Company That Buy Houses

Save Your home from Foreclosure

Working with EPS Houses simplifies the process of selling your home fast. They specialize in buying houses as-is, meaning there’s no need for repairs or renovations. Whether you’re facing foreclosure or just need quick cash, their friendly approach offers solutions like owner financing and creative financing options, allowing you to sell on your terms. With no banks needed, EPS Houses provide alternative paths such as lease options, making it easy for Florida homeowners to move forward without stress.

Selling As-Is, Selling With Tenants, and Subject-To Transactions

Beyond a simple cash sale, there are other creative financing options to avoid a foreclosure sale. Selling as-is is a popular choice because it means you don’t have to spend any money on repairs. A cash home buyer will purchase your property in its current condition.

If you have renters, you can sell with tenants in place. This is attractive to investors who want an immediate rental income. You can transfer the lease to the new owner without disrupting your tenants. This makes the process to sell my house Florida simple and straightforward.

Another option is a “subject-to” transaction, also known as owner financing or seller financing.

- Selling as-is: No repairs needed, saving you time and money.

- Sell with tenants: The buyer takes over the existing lease.

- Subject-to/Owner Financing: The buyer takes over your mortgage payments, providing a no bank needed solution.

Last-Minute Options and Government Assistance Programs

Even if the foreclosure sale is just around the corner, you may still have options. Government assistance programs can provide last-minute help. The Florida Homeowner Assistance Fund was created to help homeowners catch up on mortgage payments.

You can also seek help from a HUD-approved housing counselor. They are experts in loss mitigation and can negotiate with your lender on your behalf. These professionals can guide you through programs from the Department of Housing and Urban Development. We’ll now look at how to find legitimate help.

Finding Legit Foreclosure Prevention Help and Avoiding Scams

When you’re desperate for foreclosure prevention help, it’s easy to fall for scams. Be wary of any company that guarantees to stop your foreclosure for a hefty fee. True help is often free or low-cost.

Legitimate help comes from HUD-approved housing counseling agencies, legal aid services, and reputable attorneys. The Florida Bar Lawyer Referral Service can connect you with a qualified attorney. Always verify the credentials of anyone offering to help.

To avoid scams, follow these tips:

- Never pay an upfront fee for help with a loan modification.

- Check with the Office of Financial Regulation to ensure a company is licensed.

- Be suspicious of anyone who tells you to stop paying your mortgage servicer.

- Rely on official sources like HUD or the Attorney General’s Office.

Conclusion

In conclusion, stopping foreclosure in Florida requires a proactive approach and an understanding of your rights and options. As a homeowner, knowing the foreclosure process, gathering essential documents, and exploring immediate actions like loan modification or bankruptcy can significantly impact your situation. Additionally, consider unique solutions such as selling your home quickly or utilizing government assistance programs. Remember, you are not alone in this challenging time; there are resources and professionals available to help you navigate your options. If you need personalized assistance or guidance, don’t hesitate to get in touch. Taking the first step is crucial for regaining control over your financial future.

Frequently Asked Questions

Can I stop foreclosure immediately in Florida, and what’s the fastest way?

Yes, you can stop foreclosure immediately. Filing for bankruptcy triggers an automatic stay, which halts the foreclosure process and gives you breathing room. The other fast option is accepting a cash offer from a home buying company, which can close the sale in days and stop further legal action.

Is selling my home for cash or as-is a good solution for avoiding foreclosure in Florida?

Selling your home for cash or as-is can be an effective strategy to avoid foreclosure in Florida. It allows for a quick sale, often bypassing lengthy repairs and traditional financing hurdles, providing homeowners with immediate relief and a fresh start. Consider this option carefully.

What government or legal programs help Florida homeowners stop foreclosure in 2025?

Florida homeowners can get government assistance through programs like the Homeowner Assistance Fund (HAF) for mortgage payments. You can also get free help with loss mitigation from a HUD-approved housing counselor from the Department of Housing and Urban Development, who can explain your rights under foreclosure laws. Contact Us Now!